Correct Generalized Cross-Validation for \(l1\)-regularized Huber Ensembles#

In this notebook, we illustrate how to perform correct generalized cross-validation for \(l1\)-regularized Huber ensembles, where each base estimator takes the form

where the Huber loss is defined as

Define base estimator#

We begin by defining a scikit-learn-type base estimator of \(\ell_1\)-regularized Huber.

[1]:

import numpy as np

import scipy as sp

import sys

sys.path.append('..')

from sklearn_ensemble_cv import Ensemble

from sklearn.linear_model import Lasso, QuantileRegressor

from sklearn.base import BaseEstimator, RegressorMixin

class HuberL1Reg(RegressorMixin, BaseEstimator):

'''

L1-regularized Huber estimator is defined as

argmin_beta sum_i loss(y_i - x_i^T beta; mu) + sum_j reg(beta_j)

where

loss(z; mu) = z^2/(2*mu) * 1{|z|<=mu} + (|z| - mu/2) * 1{|z|>mu}

reg(z) = |z|

'''

def __init__(self, lam, mu):

assert lam>0

if mu == 0:

self.reg = QuantileRegressor(quantile=0.5, alpha=0.5*lam, fit_intercept=False, solver='highs')

else:

assert mu>0

self.reg = Lasso(alpha=mu*lam, tol=1e-8, max_iter=10000, fit_intercept=False)

self.fit_intercept = False

self.lam = lam # l1-regularization parameter

self.mu = mu # Huber loss parameter

self.is_fitted_ = False

def fit(self, X, y):

n, p = X.shape

if self.mu == 0:

self.coef_ = self.reg.fit(X=X, y=y).coef_

else:

X_new = np.concatenate((X, self.lam * np.eye(n)), axis=1)

self.coef_ = self.reg.fit(X=X_new*np.sqrt(n), y=y*np.sqrt(n)).coef_[0:p]

self.is_fitted_ = True

return self

def predict(self, X):

return X @ self.coef_

def _deriv(self, r):

"""

Compute the derivative of the loss function:

loss'(r; mu) = r/mu * 1{|r|<=mu} + sign(r) * 1{|r|>mu}.

Parameters:

r : array-like, shape (n_samples,)

Residuals.

Returns:

deriv : array, shape (n_samples,)

Derivative of the loss function.

"""

return np.where(np.abs(r)<self.mu, r/self.mu, np.sign(r))

def _dof(self, eps=1e-12):

"""

Compute the degrees of freedom.

Parameters:

eps : float, optional (default=1e-12)

Threshold for considering coefficients as non-zero.

Returns:

dof : int

Degrees of freedom.

"""

return np.sum(np.abs(self.coef_)>eps)

def get_gcv_input(self, X, y):

"""

Get inputs for Generalized Cross-Validation (GCV).

Parameters:

X : array-like, shape (n_samples, n_features)

Training data.

y : array-like, shape (n_samples,)

Target values.

Returns:

r : array, shape (n_samples,)

Residuals.

loss_p : array, shape (n_samples,)

First derivative of the loss function.

dof : int

Degrees of freedom.

tr_V : float

Trace of the influence matrix.

"""

r = y.reshape(-1) - self.predict(X).reshape(-1)

loss_p = self._deriv(r)

loss_pp = np.abs(r)<self.mu

dof = self._dof()

tr_V = (np.sum(loss_pp) - dof)/ self.mu

return r, loss_p, dof, tr_V

Note that, we have defined an extra function get_gcv_input that returns the quantities needed for the GCV computation. Later, sklearn_ensemble_cv package can use this function to perform cross-validation for the \(\ell_1\)-regularized Huber ensemble.

Function for risk estimation and cross-validation#

Next, we define a function that takes in the following parameters:

the number of subsamples

k, the number of samplesn, the number of featuresp;the sparsity level

s, the degrees of freedom of t-distributed noisesdof;random seed

seedand the number of base estimatorsM;

and returns the risk of the ensemble and the GCV score.

[2]:

def compute_risk_gcv(

k, n, p,

s, dof,

lam, mu, seed, M=50):

rng = np.random.default_rng(seed)

X = rng.normal(loc=0, scale=1/np.sqrt(p), size=(n, p))

theta = np.hstack([np.zeros(int(p*s)), np.ones(p-int(p*s))]) * rng.normal(loc=0, scale=1, size=p)

z = rng.standard_t(df=dof, size=n)

y = X @ theta + z

X_test = rng.normal(loc=0, scale=1/np.sqrt(p), size=(n, p))

y_test = X_test @ theta

kwargs_regr = {'lam': lam, 'mu': mu}

kwargs_ensemble = {'max_samples':int(k), 'bootstrap': False, 'n_jobs':-1}

regr = Ensemble(estimator=HuberL1Reg(**kwargs_regr), n_estimators=M, **kwargs_ensemble)

regr.fit(X, y)

risk_gcv = regr.compute_cgcv_estimate(X, y)

noise = np.mean(z**2) # subtract noises to get excess risk

res_gcv = np.r_[[p/n, p/k, seed], risk_gcv - noise]

risks = regr.compute_risk(X_test, y_test)

res_est = np.r_[[p/n, p/k, seed], risks]

return res_gcv, res_est

Simualtion#

[3]:

import os

import numpy as np

import seaborn as sns

from joblib import Parallel, delayed

import matplotlib.pyplot as plt

import pandas as pd

sns.set()

s = 0.1 # sparsity of signal

lam = 0.5

mu = 1

dist = 't-5'; dof = 5

delta = 10;phi=1/delta

cs = np.sort(np.unique((

1/delta / np.round(np.logspace(-1, 1, 10), 2))))

cs = cs[1/(delta*cs)<=6.]

p = 500

n = int(delta*p)

params = [{'k': k, 'n':n, 'p':p, 's':s,'dof':dof, 'lam':lam, 'mu':mu, 'seed': seed}

for k in (cs*n).astype(int) for seed in range(20)

]

print('about to start parallel jobs:', len(params))

res = Parallel(n_jobs=5, verbose=1)(

delayed(compute_risk_gcv)(**d) for d in params)

res_gcv, res_est = list(zip(*res))

res_gcv = pd.DataFrame(res_gcv, columns=['pho', 'psi', 'seed'] + ['R-{}'.format(M) for M in range(1,51)])

res_est = pd.DataFrame(res_est, columns=['pho', 'psi', 'seed'] + ['R-{}'.format(M) for M in range(1,51)])

about to start parallel jobs: 180

[Parallel(n_jobs=5)]: Using backend LokyBackend with 5 concurrent workers.

[Parallel(n_jobs=5)]: Done 40 tasks | elapsed: 23.3s

[Parallel(n_jobs=5)]: Done 180 out of 180 | elapsed: 8.3min finished

[4]:

res_gcv = pd.wide_to_long(res_gcv, stubnames='R', i=['psi', 'seed'], j='M', sep='-', suffix=r'.*').reset_index()

res_est = pd.wide_to_long(res_est, stubnames='R', i=['psi', 'seed'], j='M', sep='-', suffix=r'.*').reset_index()

res_est['type'] = 'est'

res_gcv['type'] = 'gcv'

res = pd.concat([res_gcv, res_est], axis=0).reset_index()

[5]:

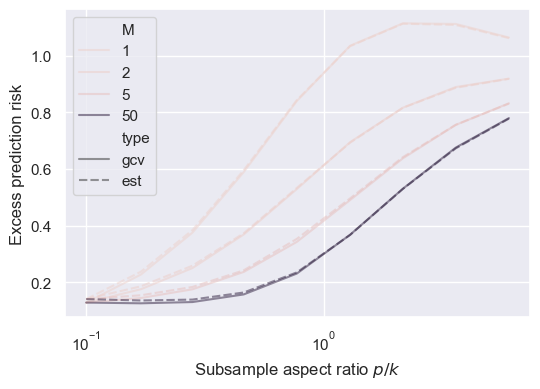

fig, ax = plt.subplots(1, 1, figsize=(6, 4))

sns.lineplot(res[res['M'].isin([1,2,5,50])], x='psi', y='R', hue='M', style='type', alpha=0.5, errorbar=None, ax=ax)

ax.set_xscale('log')

ax.set_xlabel('Subsample aspect ratio $p/k$')

ax.set_ylabel('Excess prediction risk')

[5]:

Text(0, 0.5, 'Excess prediction risk')