This page was generated from

docs/tutorials/gcv.ipynb.

Interactive online version:

.

.

Generalized Cross-Validation for Non-Ensemble Models#

[1]:

import sys

sys.path.append('..')

import os

n_cores = int(8)

os.environ["OMP_NUM_THREADS"] = f"{n_cores}"

os.environ["OPENBLAS_NUM_THREADS"] = f"{n_cores}"

os.environ["MKL_NUM_THREADS"] = f"{n_cores}"

os.environ["VECLIB_MAXIMUM_THREADS"] = f"{n_cores}"

os.environ["NUMEXPR_NUM_THREADS"] = f"{n_cores}"

os.environ["NUMBA_CACHE_DIR"]='/tmp/numba_cache'

import numpy as np

from sklearn_ensemble_cv import reset_random_seeds

import matplotlib.pyplot as plt

reset_random_seeds(0)

GCV for risk estimation#

[2]:

from sklearn.linear_model import Ridge, Lasso, ElasticNet

from sklearn_ensemble_cv import generate_data, Ensemble

reset_random_seeds(0)

n_samples, n_features = 1000, 800

Sigma, beta0, X_train, y_train, X_test, y_test, _, _ = generate_data(

n_samples, n_features, coef='random', func='quad', sigma_quad=.1,

rho_ar1=0., sigma=.5, df=np.inf, n_test=1000,

)

kwargs_regr = {'alpha': 0.01*X_train.shape[0], 'fit_intercept':False}

kwargs_ensemble = {'max_samples': 0.5, 'bootstrap':False}

regr = Ensemble(estimator=Ridge(**kwargs_regr), n_estimators=1, **kwargs_ensemble)

regr = regr.fit(X_train, y_train)

[3]:

df_gcv = regr.compute_gcv_estimate(X_train, y_train, M0=1, type='union', return_df=True)

df_gcv

[3]:

| M | estimate | err_train | deno | |

|---|---|---|---|---|

| 0 | 1 | 0.986995 | 0.000927 | 0.00094 |

[4]:

df_risk = regr.compute_risk(X_test, y_test, return_df=True)

df_risk

[4]:

| M | risk | |

|---|---|---|

| 0 | 1 | 1.015682 |

GCV for tuning regularization parameters#

[5]:

from sklearn_ensemble_cv import GCV

grid_regr = {'alpha': np.logspace(-3, 0, 10)*X_train.shape[0]}

grid_ensemble = {'max_samples': 1., 'bootstrap':False}

res_gcv, info_gcv = GCV(

X_train, y_train, Ridge, grid_regr, grid_ensemble,

M=1, M0=1, corrected=True, type='full', return_df=True, X_test=X_test, Y_test=y_test,

)

[6]:

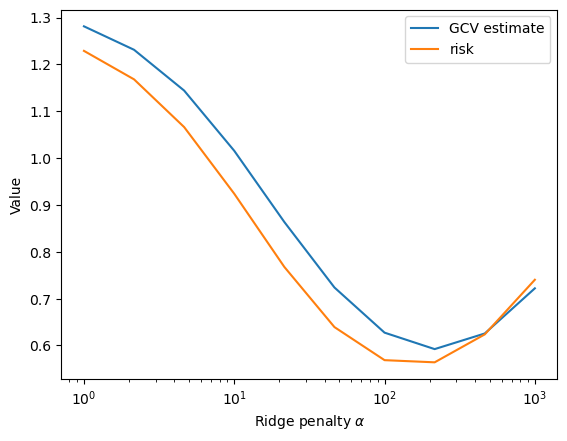

res_gcv

[6]:

| alpha | risk_val-1 | risk_val-inf | risk_test-1 | |

|---|---|---|---|---|

| 0 | 1.000000 | 1.281178 | NaN | 1.228796 |

| 1 | 2.154435 | 1.231096 | NaN | 1.167976 |

| 2 | 4.641589 | 1.144019 | NaN | 1.066096 |

| 3 | 10.000000 | 1.015488 | NaN | 0.923820 |

| 4 | 21.544347 | 0.863445 | NaN | 0.767550 |

| 5 | 46.415888 | 0.723675 | NaN | 0.639160 |

| 6 | 100.000000 | 0.627298 | NaN | 0.568579 |

| 7 | 215.443469 | 0.592169 | NaN | 0.563968 |

| 8 | 464.158883 | 0.625508 | NaN | 0.623591 |

| 9 | 1000.000000 | 0.721912 | NaN | 0.740226 |

[7]:

info_gcv

[7]:

{'best_params_regr': {'alpha': np.float64(215.44346900318823)},

'best_params_ensemble': {'random_state': 0,

'max_samples': 1.0,

'bootstrap': False,

'n_estimators': 1},

'best_n_estimators': np.int64(1),

'best_params_index': np.int64(7),

'best_score': np.float64(0.5921689022419518)}

[8]:

res_gcv.iloc[info_gcv['best_params_index']]['risk_test-{}'.format(info_gcv['best_n_estimators'])]

[8]:

np.float64(0.5639675571939373)

[9]:

plt.plot(res_gcv['alpha'], res_gcv['risk_val-1'], label='GCV estimate')

plt.plot(res_gcv['alpha'], res_gcv['risk_test-1'], label='risk')

plt.xscale('log')

plt.xlabel(r'Ridge penalty $\alpha$')

plt.ylabel('Value')

plt.legend()

plt.show()

[ ]: